Python Backtesting with Monte Carlo, Equity Curve and More

Tschechien

Englisch

Einige Informationen werden in englischer Sprache angezeigt.

Über mich

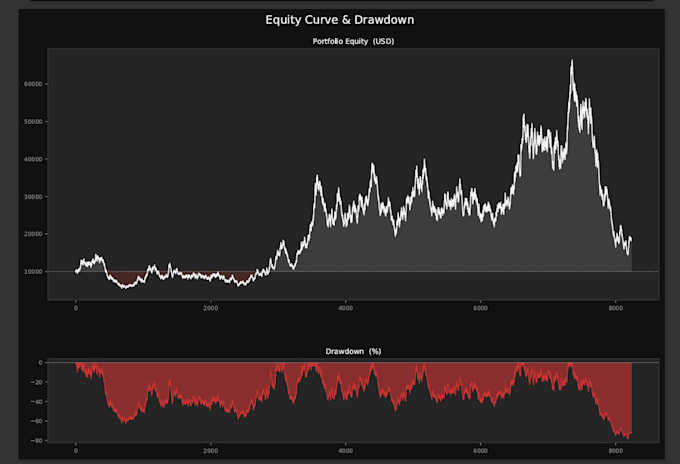

I'm a quantitative trader and Python developer specializing in algorithmic strategy backtesting. I build vectorized backtesting pipelines that test your trading strategy on years of historical data — giving you statistically reliable results, not just curve-fitted hopes. My reports include equity curves, drawdown analysis, Monte Carlo simulations, and optimal position sizing via Kelly Criterion.... Mehr lesen